New Strategy : The Right Way to Increase Domain Authority DA Scores 2024

Tips and technic as new strategy to increase domain Authority or DA scores in 2024 : Whether you’re a seasoned…

Read Our View On Every News

Headline News

Headline News

Tips and technic as new strategy to increase domain Authority or DA scores in 2024 : Whether you’re a seasoned…

Branded Short Domain Or Exact Match Domain names : Numerous pivotal decisions need to be made when you first start…

Most new entrepreneurs don’t think about their startup name too much but it’s a big deal. Choosing the right name…

One of the earliest steps you’ll take for your business is choosing and securing a domain – an identifying name…

Many people dream of starting their own business, but only a fraction of those people take the leap and throw…

Investor frenzy over artificial intelligence boosted shares of Leeno Industrial, an under-the-radar semiconductor company in South Korea, by more than…

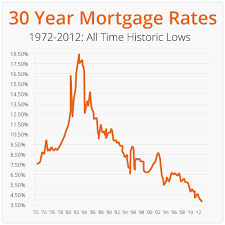

The average APR for the benchmark 30-year fixed-rate mortgage rose to 7.26% today from 7.22% yesterday. This time last week,…

SeeHeadlines.com – Back in 2021, as the market for venture capital funding of fintech companies was peaking, San Francisco Bay Area…

All brands likely want a captivated and devout social media following. Why wouldn’t they? It’s a low-cost way to increase brand…

2023 has been a transformative one for marketers. Creating content has never been easier with artificial intelligence, and as PPC…